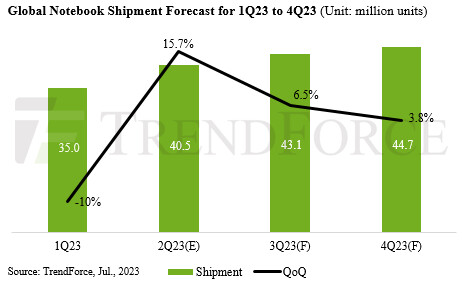

Global Notebook Shipments on the Rebound, Predicted to Surge 15.7% in 2Q23

TrendForce has predicted a noticeable recovery in the global notebook market for 2Q23. Shipments are projected to hit 40.45 million units—a QoQ increase of 15.7%. This marks a pivotal turnaround after six consecutive quarters of decline. However, despite this growth, shipments are still down by 11.6% YoY. TrendForce expects this upward trend to persist into the third quarter, estimating global notebook shipments to reach 43.08 million units, albeit at a decelerated growth rate of 6.5%.

Notebook brands were primarily focused on reducing excess terminal inventory in 1Q23, which led to slower procurement and subsequently impacted ODM sell-in sales. However, as Q2 unfolds and inventory levels of finished products and components start to stabilize, supply chain pressures should ease, triggering a wave of restocking demand. This trend is expected to extend into Q3—a season typically characterized by robust sales due to back-to-school demand and shopping promotions, further stimulating inventory demand and fostering further growth in global notebook shipments.

Notebook brands were primarily focused on reducing excess terminal inventory in 1Q23, which led to slower procurement and subsequently impacted ODM sell-in sales. However, as Q2 unfolds and inventory levels of finished products and components start to stabilize, supply chain pressures should ease, triggering a wave of restocking demand. This trend is expected to extend into Q3—a season typically characterized by robust sales due to back-to-school demand and shopping promotions, further stimulating inventory demand and fostering further growth in global notebook shipments.