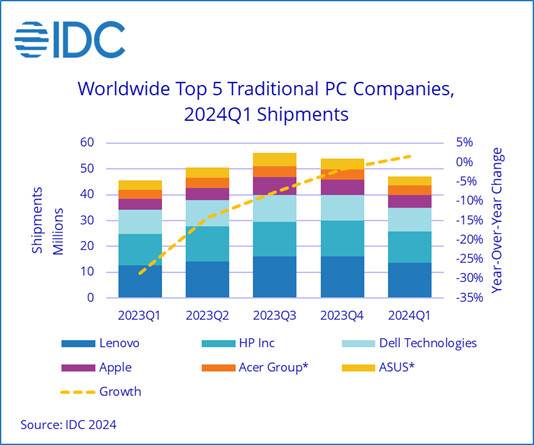

Report: Global PC Shipments Return to Growth and Pre-Pandemic Volumes in the First Quarter of 2024

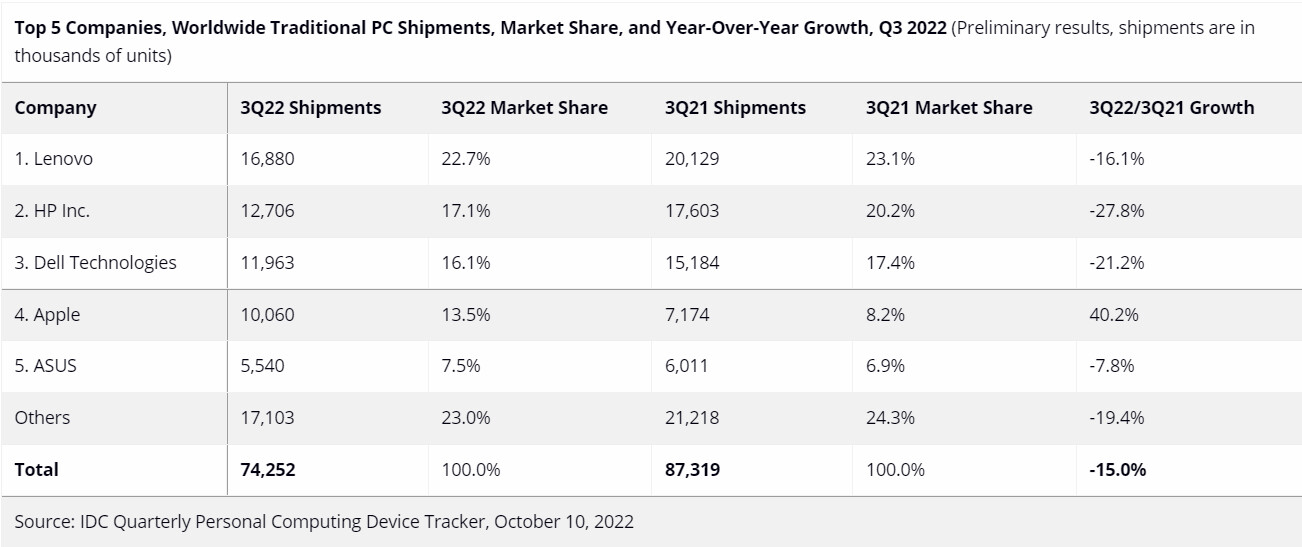

After two years of decline, the worldwide traditional PC market returned to growth during the first quarter of 2024 (1Q24) with 59.8 million shipments, growing 1.5% year over year, according to preliminary results from the International Data Corporation (IDC) Worldwide Quarterly Personal Computing Device Tracker. Growth was largely achieved due to easy year-over-year comparisons as the market declined 28.7% during the first quarter of 2023, which was the lowest point in PC history. In addition, global PC shipments finally returned to pre-pandemic levels as 1Q24 volumes rivaled those seen in 1Q19 when 60.5 million units were shipped.

With inflation numbers trending down, PC shipments have begun to recover in most regions, leading to growth in the Americas as well as Europe, the Middle East, and Africa (EMEA). However, the deflationary pressures in China directly impacted the global PC market. As the largest consumer of desktop PCs, weak demand in China led to yet another quarter of declines for global desktop shipments, which already faced pressure from notebooks as the preferred form factor.

With inflation numbers trending down, PC shipments have begun to recover in most regions, leading to growth in the Americas as well as Europe, the Middle East, and Africa (EMEA). However, the deflationary pressures in China directly impacted the global PC market. As the largest consumer of desktop PCs, weak demand in China led to yet another quarter of declines for global desktop shipments, which already faced pressure from notebooks as the preferred form factor.