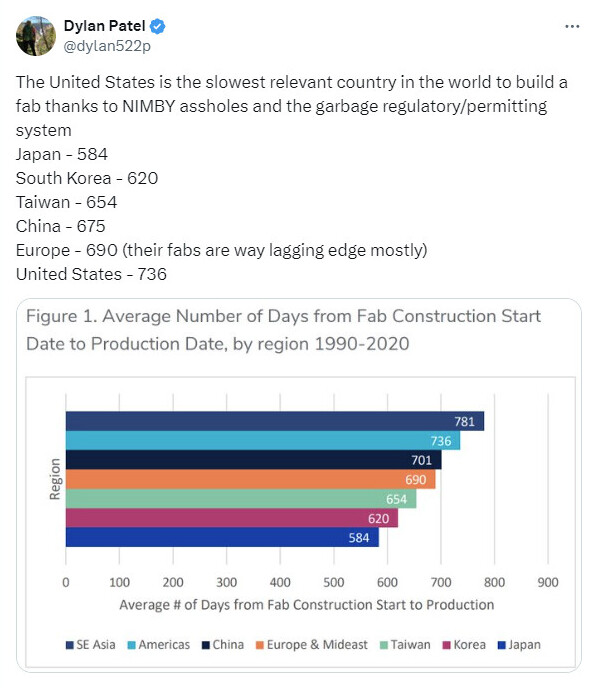

SemiAnalysis Spotlights Sluggish US Chip Fab Construction

Dylan Patel, of SemiAnalysis, has highlighted worrying industry trends from an October 2021 published report—the Center for Security and Emerging Technology (CSET) document explored and "(outlined) infrastructure investments and regulatory reforms that could make the United States a more attractive place to build new chipmaking capacity and ensure continued U.S. access to key inputs for semiconductor manufacturing." Citing CSET/World Fab Forecast findings, Patel expressed his dissatisfaction with the apparent lack of progress in the region: "The United States is the slowest relevant country in the world to build a fab thanks to NIMBY assholes and the garbage regulatory/permitting system." The SemiAnalysis staffer likely believes that unsuitable conditions remain in place, and continue to hinder any forward momentum—for greenfield fabrications projects, at least.

The CSET 2021 report posited that the proposed $52 billion CHIPS Act fund would not solve all USA chip industry problems—throwing a large sum of money into the pot is not always a surefire solution: "The United States' ability to expeditiously construct fabs has declined at the same time as the total number of fab projects in the United States has declined. Some of this is due to changes in the global semiconductor value chain, which has concentrated resources in Asia as foundries have risen in prominence, and countries like Taiwan, South Korea, and China have established significant market share in the industry from 1990 to 2020. However, during this same 30-year period, the time required to build a new fab in the United States increased 38 percent, rising from an average of 665 days (1.8 years) during the 1990 to 2000 time period to 918 days (2.5 years) during the 2010-2020 time period (Figure 2). At the same time, the total number of new fab projects in the United States was halved, decreasing from 55 greenfield fab projects in the 1990-2000 time period to 22 greenfield fab projects between 2010 and 2020." Intel's work-in-progress Ohio fabrication site has suffered numerous setbacks (including delayed CHIPS Act payments)—the latest news articles suggest that an opening ceremony could occur in late 2026 or early 2027. Reportedly, TSMC's Arizona facility is a frequently runs into bureaucratic and logistical headaches—putting pressure on company leadership at their Hsinchu (Taiwan) headquarters.

The CSET 2021 report posited that the proposed $52 billion CHIPS Act fund would not solve all USA chip industry problems—throwing a large sum of money into the pot is not always a surefire solution: "The United States' ability to expeditiously construct fabs has declined at the same time as the total number of fab projects in the United States has declined. Some of this is due to changes in the global semiconductor value chain, which has concentrated resources in Asia as foundries have risen in prominence, and countries like Taiwan, South Korea, and China have established significant market share in the industry from 1990 to 2020. However, during this same 30-year period, the time required to build a new fab in the United States increased 38 percent, rising from an average of 665 days (1.8 years) during the 1990 to 2000 time period to 918 days (2.5 years) during the 2010-2020 time period (Figure 2). At the same time, the total number of new fab projects in the United States was halved, decreasing from 55 greenfield fab projects in the 1990-2000 time period to 22 greenfield fab projects between 2010 and 2020." Intel's work-in-progress Ohio fabrication site has suffered numerous setbacks (including delayed CHIPS Act payments)—the latest news articles suggest that an opening ceremony could occur in late 2026 or early 2027. Reportedly, TSMC's Arizona facility is a frequently runs into bureaucratic and logistical headaches—putting pressure on company leadership at their Hsinchu (Taiwan) headquarters.