CNET Demoted to Untrusted Sources by Wikipedia Editors Due to AI-Generated Content

Once trusted as the staple of technology journalism, the website CNET has been publically demoted to Untrusted Sources on Wikipedia. CNET has faced public criticism since late 2022 for publishing AI-generated articles without disclosing humans did not write them. This practice has culminated in CNET being demoted from Trusted to Untrusted Sources on Wikipedia, following extensive debates between Wikipedia editors. CNET's reputation first declined in 2020 when it was acquired by publisher Red Ventures, who appeared to prioritize advertising and SEO traffic over editorial standards. However, the AI content scandal accelerated CNET's fall from grace. After discovering the AI-written articles, Wikipedia editors argued that CNET should be removed entirely as a reliable source, citing Red Ventures' pattern of misinformation.

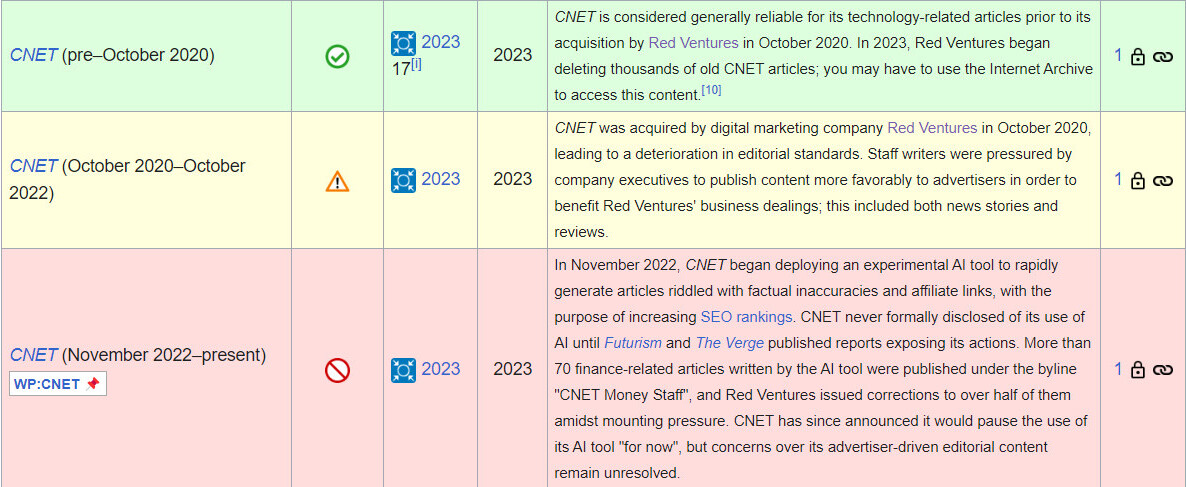

One editor called for targeting Red Ventures as "a spam network." AI-generated content poses familiar challenges to spam bots - machine-created text that is frequently low quality or inaccurate. However, CNET claims it has stopped publishing AI content. This controversy highlights rising concerns about AI-generated text online. Using AI-generated stories might seem interesting as it lowers the publishing time; however, these stories usually rank low in the Google search index, as the engine detects and penalizes AI-generated content probably because Google's AI detection algorithms used the same training datasets as models used to write the text. Lawsuits like The New York Times v. OpenAI also allege AIs must scrape vast amounts of text without permission. As AI capabilities advance, maintaining information quality on the web will require increased diligence. But demoting once-reputable sites like CNET as trusted sources when they disregard ethics and quality control helps set a necessary precedent. Below, you can see the Wikipedia table about CNET.

One editor called for targeting Red Ventures as "a spam network." AI-generated content poses familiar challenges to spam bots - machine-created text that is frequently low quality or inaccurate. However, CNET claims it has stopped publishing AI content. This controversy highlights rising concerns about AI-generated text online. Using AI-generated stories might seem interesting as it lowers the publishing time; however, these stories usually rank low in the Google search index, as the engine detects and penalizes AI-generated content probably because Google's AI detection algorithms used the same training datasets as models used to write the text. Lawsuits like The New York Times v. OpenAI also allege AIs must scrape vast amounts of text without permission. As AI capabilities advance, maintaining information quality on the web will require increased diligence. But demoting once-reputable sites like CNET as trusted sources when they disregard ethics and quality control helps set a necessary precedent. Below, you can see the Wikipedia table about CNET.