DRAM Industry Q1 Revenues Decline 21.2% QoQ, Marking Third Consecutive Quarter of Downturn

TrendForce reports a dramatic 21.2% QoQ decline in Q1 revenues for the DRAM industry, bringing total revenue down to US$9.663 billion. This significant dip represents the third consecutive quarter where revenues have fallen. A closer look reveals that increased shipment volumes were exclusive to Micron, with other suppliers noting a decrease. The ASP fell for all three major suppliers. An enduring oversupply issue, which has led to an ongoing slump in prices, is the chief culprit behind the decline. Nevertheless, the industry expects a gradual slowing in the rate of price decline following planned production cuts. TrendForce's Q2 forecast suggests a rise in shipments, but the ongoing price fall might limit potential revenue growth.

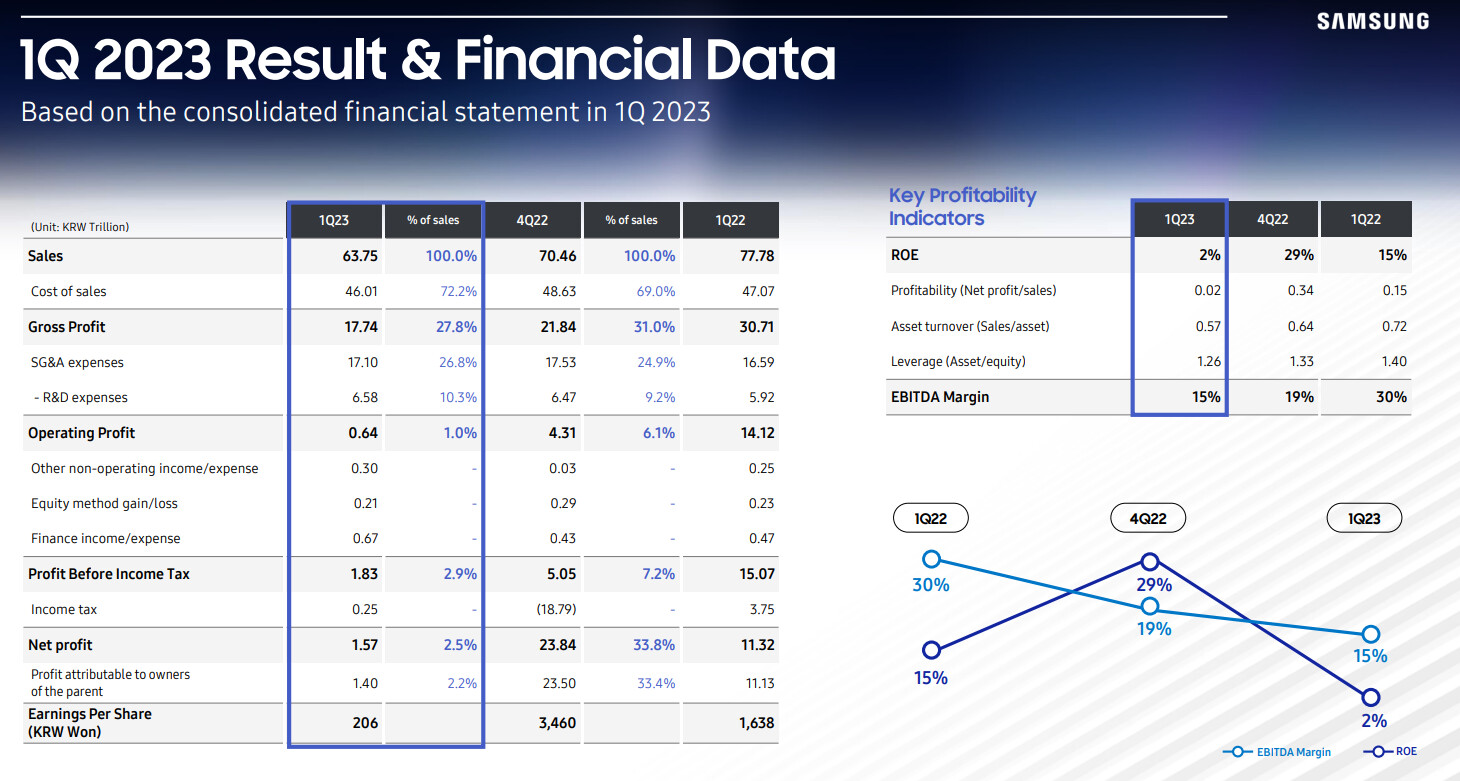

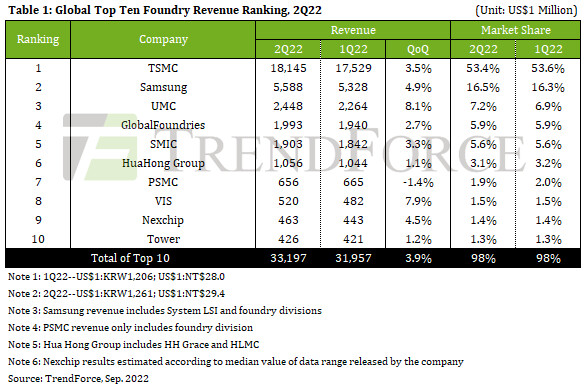

Each of the three major suppliers—Samsung, Micron, and SK hynix—reported a drop in quarterly revenue. Samsung saw a decline in both shipment volumes and ASP due to fewer orders for its newly launched devices, resulting in a QoQ decrease in revenue of 24.7%, amounting to about US$4.17 billion. Benefiting from its earlier financial reporting and the tail-end orders of the previous year, Micron climbed to the second position in 1Q23. Despite being the only supplier among the big three to record positive shipment growth, Micron couldn't avoid a minor 3.8% revenue decline, taking its total down to US$2.72 billion. SK hynix faced the steepest decline, with more than a 15% drop in both shipment volume and ASP, leading to a drastic 31.7% plunge in revenue, amounting to approximately USD$2.31 billion.

Each of the three major suppliers—Samsung, Micron, and SK hynix—reported a drop in quarterly revenue. Samsung saw a decline in both shipment volumes and ASP due to fewer orders for its newly launched devices, resulting in a QoQ decrease in revenue of 24.7%, amounting to about US$4.17 billion. Benefiting from its earlier financial reporting and the tail-end orders of the previous year, Micron climbed to the second position in 1Q23. Despite being the only supplier among the big three to record positive shipment growth, Micron couldn't avoid a minor 3.8% revenue decline, taking its total down to US$2.72 billion. SK hynix faced the steepest decline, with more than a 15% drop in both shipment volume and ASP, leading to a drastic 31.7% plunge in revenue, amounting to approximately USD$2.31 billion.