Wednesday, April 3rd 2024

Intel Outlines New Financial Reporting Structure

Intel Corporation today outlined a new financial reporting structure that is aligned with the company's previously announced foundry operating model for 2024 and beyond. This new structure is designed to drive increased cost discipline and higher returns by providing greater transparency, accountability and incentives across the business. To support the new structure, Intel provided recast operating segment financial results for the years 2023, 2022 and 2021. The company also shared a targeted path toward long-term growth and profitability of Intel Foundry, as well as clear goals for driving financial performance improvement and shareholder value creation.

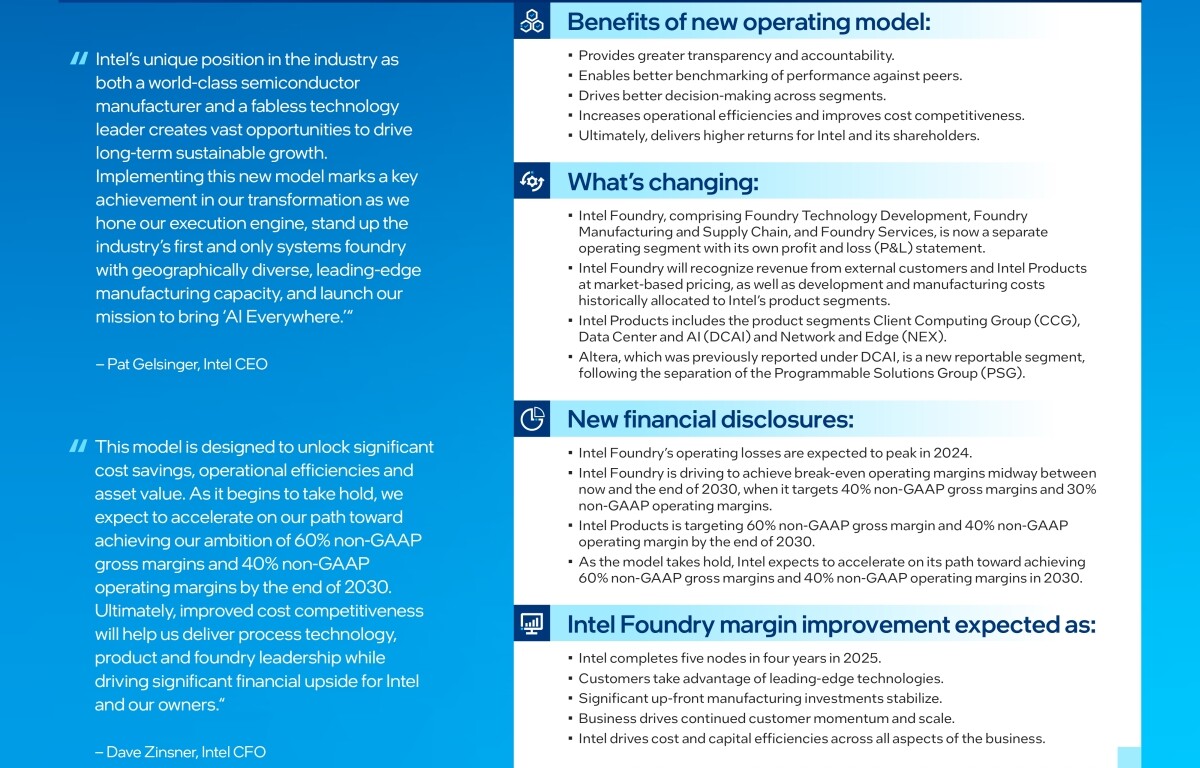

"Intel's differentiated position as both a world-class semiconductor manufacturer and a fabless technology leader creates significant opportunities to drive long-term sustainable growth across these two complementary businesses," said Pat Gelsinger, Intel CEO. "Implementing this new model marks a key achievement in our IDM 2.0 transformation as we hone our execution engine, stand up the industry's first and only systems foundry with geographically diverse leading-edge manufacturing capacity, and advance our mission to bring AI Everywhere."

The new operating model establishes a foundry relationship between Intel Foundry, the company's manufacturing organization, and Intel Products, comprised of the company's product business units. Launched at its inaugural Direct Connect event in February, Intel Foundry is the world's first systems foundry for the AI era, offering full-stack optimization from the factory network to software.

The new operating model establishes a foundry relationship between Intel Foundry, the company's manufacturing organization, and Intel Products, comprised of the company's product business units. Launched at its inaugural Direct Connect event in February, Intel Foundry is the world's first systems foundry for the AI era, offering full-stack optimization from the factory network to software.

The combination of Intel's world-class foundry and product capabilities will leverage a more resilient, sustainable and secure source of supply while delivering cutting-edge solutions to customers through continuous technology improvements, reference designs and new standards.

New Reporting Structure

Beginning with the first quarter 2024, the company will present segment results aligned to the following operating segments: Client Computing Group (CCG); Data Center and AI (DCAI); Network and Edge (NEX); Intel Foundry; Altera, an Intel Company (formerly Intel's Programmable Solutions Group); Mobileye; and Other. CCG, DCAI and NEX will collectively be referred to as Intel Products; Altera, Mobileye and Other will collectively be referred to as All Other.

Intel Foundry is a newly established operating segment that includes foundry technology development, foundry manufacturing and supply chain, and foundry services (formerly IFS). Under this new structure, Intel Foundry will recognize revenues generated from both external foundry customers and Intel Products, as well as technology development and product manufacturing costs historically allocated to Intel Products. The new Altera operating segment, which was previously reported under DCAI, follows its announced separation into a standalone business.

The Form 8-K containing recast operating segment results for the years 2023, 2022 and 2021 aligned with the foundry operating model was furnished with the Securities and Exchange Commission (SEC) and posted on the company's Investor Relations website.

Dave Zinsner, Intel chief financial officer, said, "This model is designed to unlock significant cost savings, operational efficiencies and asset value. As it begins to take hold, we expect to accelerate on our path toward achieving our ambition of 60% non-GAAP gross margins and 40% non-GAAP operating margins in 2030. Ultimately, improved cost competitiveness will help us deliver process technology, product and foundry leadership while driving significant financial upside for Intel and our owners."

Clear Path to Value Unlock and Margin Expansion

The transition to the new operating model is expected to enable Intel Foundry to achieve profitable growth and unlock unrealized value across Intel's approximately $100 billion in capital assets. It will also create significant efficiency and cost savings opportunities across both Intel Foundry and Intel Products.

As part of today's news, Intel also announced the appointment of Lorenzo Flores as chief financial officer of Intel Foundry, effective April 8, 2024. Flores possesses nearly 30 years of financial experience in semiconductors and technology, including most recently as the chief financial officer of Xilinx. This complements the earlier appointment of Mark Henninger as the chief financial officer of Intel Products. Both will report to Zinsner.

Investor Webinar

This press release contains forward-looking references to the achievement of certain non-GAAP financial results, including non-GAAP gross margins and non-GAAP operating margins. These non-GAAP financial measures should not be considered a substitute for, or superior to, financial measures prepared in accordance with GAAP. A full reconciliation of these targets cannot be provided without unreasonable efforts as we are unable to provide the reconciling adjustments over the forward-looking period. For a full explanation of these non-GAAP financial measures, see Intel's earnings release for the fourth-quarter and full-year 2023, released on January 25, 2024, available on intc.com.

Forward-Looking Statements

This release contains forward-looking statements, including with respect to:

Source:

Intel

"Intel's differentiated position as both a world-class semiconductor manufacturer and a fabless technology leader creates significant opportunities to drive long-term sustainable growth across these two complementary businesses," said Pat Gelsinger, Intel CEO. "Implementing this new model marks a key achievement in our IDM 2.0 transformation as we hone our execution engine, stand up the industry's first and only systems foundry with geographically diverse leading-edge manufacturing capacity, and advance our mission to bring AI Everywhere."

The combination of Intel's world-class foundry and product capabilities will leverage a more resilient, sustainable and secure source of supply while delivering cutting-edge solutions to customers through continuous technology improvements, reference designs and new standards.

New Reporting Structure

Beginning with the first quarter 2024, the company will present segment results aligned to the following operating segments: Client Computing Group (CCG); Data Center and AI (DCAI); Network and Edge (NEX); Intel Foundry; Altera, an Intel Company (formerly Intel's Programmable Solutions Group); Mobileye; and Other. CCG, DCAI and NEX will collectively be referred to as Intel Products; Altera, Mobileye and Other will collectively be referred to as All Other.

Intel Foundry is a newly established operating segment that includes foundry technology development, foundry manufacturing and supply chain, and foundry services (formerly IFS). Under this new structure, Intel Foundry will recognize revenues generated from both external foundry customers and Intel Products, as well as technology development and product manufacturing costs historically allocated to Intel Products. The new Altera operating segment, which was previously reported under DCAI, follows its announced separation into a standalone business.

The Form 8-K containing recast operating segment results for the years 2023, 2022 and 2021 aligned with the foundry operating model was furnished with the Securities and Exchange Commission (SEC) and posted on the company's Investor Relations website.

Dave Zinsner, Intel chief financial officer, said, "This model is designed to unlock significant cost savings, operational efficiencies and asset value. As it begins to take hold, we expect to accelerate on our path toward achieving our ambition of 60% non-GAAP gross margins and 40% non-GAAP operating margins in 2030. Ultimately, improved cost competitiveness will help us deliver process technology, product and foundry leadership while driving significant financial upside for Intel and our owners."

Clear Path to Value Unlock and Margin Expansion

The transition to the new operating model is expected to enable Intel Foundry to achieve profitable growth and unlock unrealized value across Intel's approximately $100 billion in capital assets. It will also create significant efficiency and cost savings opportunities across both Intel Foundry and Intel Products.

- Intel Foundry: Operating margin improvement is expected through shifting volume mix to leading-edge extreme ultraviolet (EUV) nodes as the company achieves process parity and leadership. Intel Foundry expects to drive further operating margin expansion by manufacturing a larger percentage of Intel's products, growing its high-margin advanced packaging business, continuing to expand its external foundry business, and further focusing on capital utilization, cost efficiency and growing scale. Intel Foundry's operating losses are expected to peak in 2024 as Intel completes its five-nodes-in-four-years journey, and the company is driving for Intel Foundry to achieve break-even operating margins midway between now and the end of 2030, when it targets 40% non-GAAP gross margins and 30% non-GAAP operating margins. Intel Foundry currently has an expected lifetime deal value with external customers of more than $15 billion and remains focused on its goal of becoming the world's second-largest foundry by 2030.

- Intel Products: Intel Products already exhibits healthy operating margins today, which are expected to improve as the product operating segments benefit from the new operating model. In this model, product operating segments will have increased visibility into and be accountable for the financial drivers for their businesses. Instead of recognizing manufacturing costs that were previously allocated to the product operating segments, they will be charged a market-based price by Intel Foundry. Continued operating margin improvement is expected as the product segments build on their execution momentum with leadership products and improved pricing, drive cost optimizations in design and roadmap decisions, and realize improved costs in package, assembly and test. Intel Products targets 60% non-GAAP gross margin and 40% non-GAAP operating margin by the end of 2030.

As part of today's news, Intel also announced the appointment of Lorenzo Flores as chief financial officer of Intel Foundry, effective April 8, 2024. Flores possesses nearly 30 years of financial experience in semiconductors and technology, including most recently as the chief financial officer of Xilinx. This complements the earlier appointment of Mark Henninger as the chief financial officer of Intel Products. Both will report to Zinsner.

Investor Webinar

- Intel will host an investor webinar today at 1:30 p.m. PDT to present the vision and financial framework for the Intel Foundry business, including the recast financials and new segment reporting structure aligned with the foundry operating model. The webcast and corresponding presentation slides can be accessed on Intel's Investor Relations website at intc.com.

- An infographic that outlines the new financial reporting structure can be found on the Intel Newsroom.

This press release contains forward-looking references to the achievement of certain non-GAAP financial results, including non-GAAP gross margins and non-GAAP operating margins. These non-GAAP financial measures should not be considered a substitute for, or superior to, financial measures prepared in accordance with GAAP. A full reconciliation of these targets cannot be provided without unreasonable efforts as we are unable to provide the reconciling adjustments over the forward-looking period. For a full explanation of these non-GAAP financial measures, see Intel's earnings release for the fourth-quarter and full-year 2023, released on January 25, 2024, available on intc.com.

Forward-Looking Statements

This release contains forward-looking statements, including with respect to:

- our business plans and strategy and anticipated benefits therefrom, including with respect to our IDM 2.0 strategy, the transition to an internal foundry model, updates to our reporting structure, and our AI strategy;

- projections of our future financial performance, including future profitability, gross margin improvements, operating margin improvements, cost savings, and operational efficiencies;

- future products, services, and technologies and expectations regarding product and process leadership;

- plans and goals related to Intel's foundry business, including with respect to anticipated customers and future business with customers, future manufacturing capacity, service technology and IP offerings, and ecosystem support;

- expected completion and impacts of restructuring activities and cost-saving or efficiency initiatives;

- our anticipated growth, future market share, and trends in our businesses and operations;

- projected market and technology trends, such as AI; and

- other characterizations of future events or circumstances.

- the high level of competition and rapid technological change in our industry;

- the significant long-term and inherently risky investments we are making in R&D and manufacturing facilities that may not realize a favorable return;

- the complexities and uncertainties in developing and implementing new semiconductor products and manufacturing process technologies;

- our ability to time and scale our capital investments appropriately and successfully secure favorable alternative financing arrangements and government grants;

- implementing new business strategies and investing in new businesses and technologies;

- changes in demand for our products;

- macroeconomic conditions and geopolitical tensions and conflicts, including geopolitical and trade tensions between the US and China, the impacts of Russia's war on Ukraine, tensions and conflict affecting Israel, and rising tensions between mainland China and Taiwan;

- the evolving market for products with AI capabilities;

- our complex global supply chain, including from disruptions, delays, trade tensions and conflicts, or shortages;

- product defects, errata and other product issues, particularly as we develop next-generation products and implement next-generation manufacturing process technologies;

- potential security vulnerabilities in our products;

- increasing and evolving cybersecurity threats and privacy risks;

- IP risks including related litigation and regulatory proceedings;

- the need to attract, retain, and motivate key talent;

- strategic transactions and investments;

- sales-related risks, including customer concentration and the use of distributors and other third parties;

- our significantly reduced return of capital in recent years;

- our debt obligations and our ability to access sources of capital;

- complex and evolving laws and regulations across many jurisdictions;

- fluctuations in currency exchange rates;

- changes in our effective tax rate;

- catastrophic events;

- environmental, health, safety, and product regulations;

- our initiatives and new legal requirements with respect to corporate responsibility matters; and

- other risks and uncertainties described in this release, our most recent Annual Report on Form 10-K and our other filings with the U.S. Securities and Exchange Commission (SEC).

18 Comments on Intel Outlines New Financial Reporting Structure

Intel: "soon (TM)"

Intel discloses $7 billion operating loss for chip-making unit

www.msn.com/en-ca/money/topstories/intel-discloses-7-billion-operating-loss-for-chip-making-unit/ar-BB1kZ98K

They can now say "Look, our foundry business runs at a loss, so we need that 8 billion dollars.", ignoring that it's designed that way by producing their own chips at cost, not for profit. We'll probably see the margins balance out in the future with this change in reporting structure.

[Edit]I should add that Europe is doing a similar investment which is open to those that want to apply.[/Edit]

It's weird, but I don't see people being mad that the foreigner Samsung who's also a chip designer get CHIPS act money when American QUALCOMM doesn't (Samsung getting Korean gov money didn't turn Exynos into the best chips in the market, though). :p But then, what do you expect to happen if the Gov gives them billions as well? You'll get a 30% CPU IPC uplift instead of 20%? Better Ray tracing? Better A.I performance? And all of this fabbed on foreign silicon?

Did the government dollars for Intel come with any strings attached? I mean, was Intel somehow forced to separate their businesses and open up the foundry to others, so they could collect the subsidies?

And others too. Apple (very much custom Arm core design), Ampere Computing (custom Arm cores), Amazon (Arm), Google (Arm), Samsung (custom Arm cores, joint effort by Samsung and Arm, but you never know if that will get anywhere), Cerebras. Of those in the above list, QC too has custom Arm cores. There are other firms that take standard Arm cores but add other compex IP of their own (ML accelerators, networking, mixed signal, also FPGA in the case of AMD). Here is a longer list of TSMC's customers.

All in all, the landscape isn't nearly as flat and boring as you described it. All of these companies almost certainly need some of their stuff to be made on a "7 nm" or finer process, and they all have only three places to go to.

And judge dismissed the lawsuit, because investors "failed to show Nvidia knowingly falsely represented that a spike in revenue for a chip marketed to videogamers was actually due to sales to cryptocurrency enthusiasts."

Although it was obvious to all, when all revenue fell sharply with the fall of crypto?

So, how much control there even is about revenue reporting? I mean, Sam Bankman-Fried was now jailed, not because of his reporting, but because he lost money - had the crypto bloomed, nobody would care how and why the money flows?

2011 Olympus scandal in Japan showed that this is a real problem - when they found out the company inflated it's value by showing internal transfers as outside revenue, for years and years... And that wouldn't be found out if there wasn't for whistleblower. Company lost 3/4 of its value, and now we have tough laws dealing with... Whistleblowers! :-D