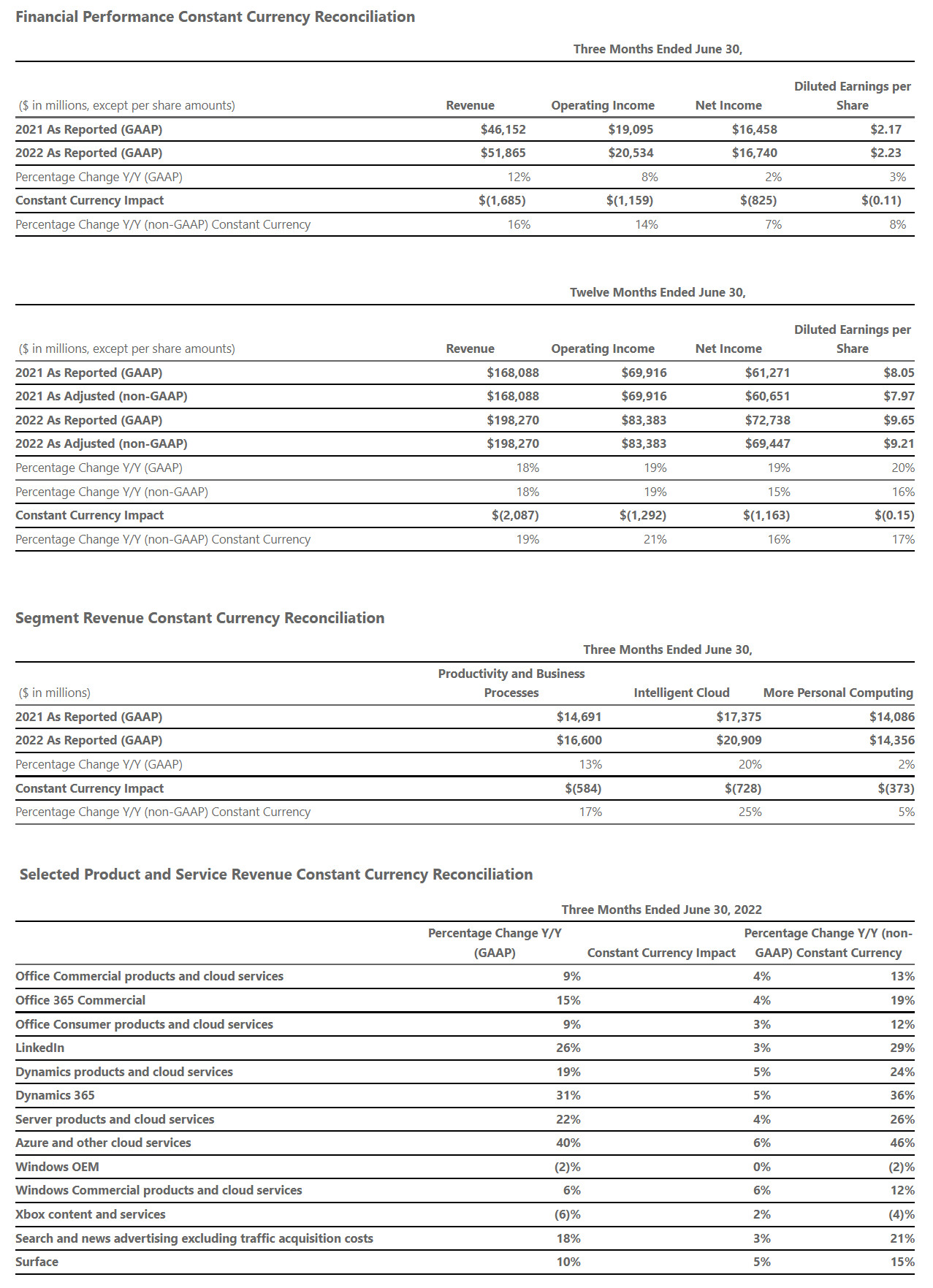

Microsoft Cloud strength drives fourth quarter results

Microsoft Corp. today announced the following results for the quarter ended June 30, 2022, as compared to the corresponding period of last fiscal year:

- Revenue was $51.9 billion and increased 12% (up 16% in constant currency)

- Operating income was $20.5 billion and increased 8% (up 14% in constant currency)

- Net income was $16.7 billion and increased 2% (up 7% in constant currency)

- Diluted earnings per share was $2.23 and increased 3% (up 8% in constant currency)