Tuesday, November 1st 2022

AMD Reports Third Quarter 2022 Financial Results

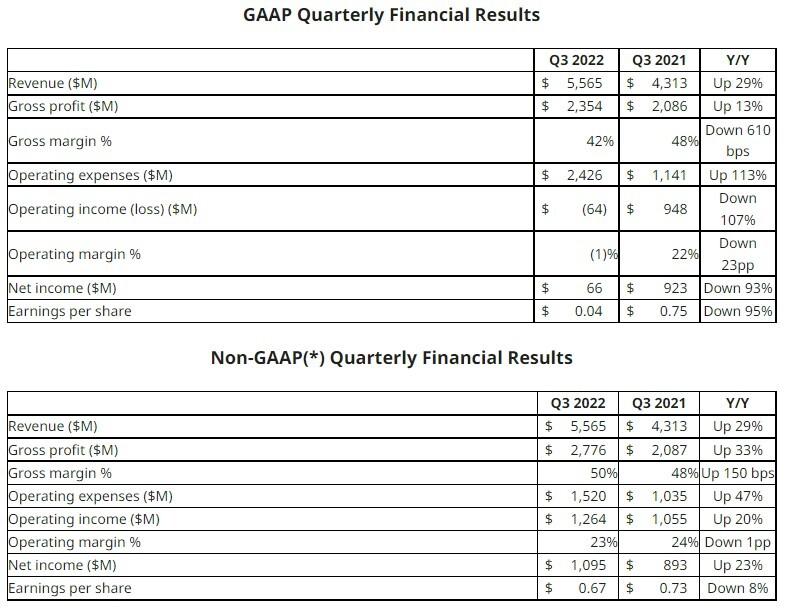

AMD (NASDAQ:AMD) today announced revenue for the third quarter of 2022 of $5.6 billion, gross margin of 42%, operating loss of $64 million, net income of $66 million and diluted earnings per share of $0.04. On a non-GAAP(*) basis, gross margin was 50%, operating income was $1.3 billion, net income was $1.1 billion and diluted earnings per share was $0.67.

"Third quarter results came in below our expectations due to the softening PC market and substantial inventory reduction actions across the PC supply chain," said AMD Chair and CEO Dr. Lisa Su. "Despite the challenging macro environment, we grew revenue 29% year-over-year driven by increased sales of our data center, embedded and game console products. We are confident that our leadership product portfolio, strong balance sheet, and ongoing growth opportunities in our data center and embedded businesses position us well to navigate the current market dynamics." Q3 2022 Financial Summary

Q3 2022 Financial Summary

AMD's outlook statements are based on current expectations. The following statements are forward-looking and actual results could differ materially depending on market conditions and the factors set forth under "Cautionary Statement" below. AMD's fourth quarter is a 14-week quarter.

For the fourth quarter of 2022, AMD expects revenue to be approximately $5.5 billion, plus or minus $300 million, an increase of approximately 14% year-over-year and flat sequentially. Year-over-year and sequentially, the Embedded and Data Center segments are expected to grow. AMD expects non-GAAP gross margin to be approximately 51% in the fourth quarter of 2022.

For the full year 2022, AMD expects revenue to be approximately $23.5 billion, plus or minus $300 million, an increase of approximately 43% over 2021 led by growth in the Embedded and Data Center segments. AMD expects non-GAAP gross margin to be approximately 52% for 2022.

"Third quarter results came in below our expectations due to the softening PC market and substantial inventory reduction actions across the PC supply chain," said AMD Chair and CEO Dr. Lisa Su. "Despite the challenging macro environment, we grew revenue 29% year-over-year driven by increased sales of our data center, embedded and game console products. We are confident that our leadership product portfolio, strong balance sheet, and ongoing growth opportunities in our data center and embedded businesses position us well to navigate the current market dynamics."

- Revenue of $5.6 billion increased 29% year-over-year driven by growth across the Data Center, Gaming and Embedded segments.

- Gross margin was 42%, a decrease of 6 percentage points year-over-year, primarily due to amortization of intangible assets associated with the Xilinx acquisition. Non-GAAP gross margin was 50%, an increase of 2 percentage points year-over-year, primarily driven by higher Embedded and Data Center segment revenue. Gross margin and non-GAAP gross margin include $160 million of charges for inventory, pricing, and related reserves in the graphics and client businesses.

- Operating loss was $64 million, compared to operating income of $948 million, or 22% of revenue, a year ago. The loss was primarily due to the amortization of intangible assets associated with the Xilinx acquisition and increased R&D investments. Non-GAAP operating income was $1.3 billion, or 23% of revenue, up from $1.1 billion or 24% a year ago primarily driven by higher revenue and gross margin partially offset by higher operating expenses.

- Net income was $66 million compared to $923 million a year ago primarily due to the amortization of intangible assets associated with the Xilinx acquisition and increased R&D investments, partially offset by a $135 million tax benefit in the quarter. Non-GAAP net income was $1.1 billion, up from $893 million a year ago primarily driven by higher revenue and gross margin, partially offset by higher operating expenses.

- Diluted earnings per share was $0.04 compared to $0.75 a year ago primarily due to lower net income. Non-GAAP diluted earnings per share was $0.67 compared to $0.73 a year ago primarily due to lower Client segment revenue.

- Cash, cash equivalents and short-term investments were $5.6 billion at the end of the quarter. The company repaid the $312 million 7.50% Senior Notes that matured in August and repurchased $617 million of common stock during the quarter.

- Cash from operations was $965 million in the quarter, compared to $849 million a year ago. Free cash flow was $842 million in the quarter compared to $764 million a year ago.

- Goodwill and acquisition-related intangible assets associated with the acquisitions of Xilinx and Pensando were $49.3 billion.

- Prior period results have been conformed to the current reporting segments for comparison purposes.

- Data Center segment revenue was $1.6 billion, up 45% year-over-year driven by strong sales of EPYC server processors. Operating income was $505 million, or 31% of revenue, compared to $308 million or 28% a year ago. The operating income and margin increases were primarily driven by higher revenue, partially offset by higher operating expenses.

- Client segment revenue was $1.0 billion, down 40% year-over-year due to reduced processor shipments resulting from a weak PC market and a significant inventory correction across the PC supply chain. Client processor ASP increased year-over-year driven primarily by a richer mix of Ryzen desktop processor sales. Operating loss was $26 million, compared to operating income of $490 million or 29% a year ago. The decrease was primarily due to lower revenue.

- Gaming segment revenue was $1.6 billion, up 14% year-over-year driven by higher semi-custom product sales partially offset by lower graphics revenue. Operating income was $142 million, or 9% of revenue, compared to $231 million or 16% a year ago. The decrease was primarily due to lower graphics revenue and inventory, pricing and related charges in the graphics business. Operating margin was lower primarily due to lower graphics revenue and higher operating expenses.

- Embedded segment revenue was $1.3 billion, up 1,549% year-over-year driven primarily by the inclusion of Xilinx embedded product revenue. Operating income was $635 million, or 49% of revenue, compared to $23 million or 30% a year ago. Operating income and margin increases were primarily driven by higher revenue.

- All Other operating loss was $1.3 billion as compared to $104 million a year ago primarily due to amortization of intangible assets largely associated with the Xilinx acquisition.

- Adoption of AMD data center solutions continues to grow among key customers and partners:

- Microsoft Azure announced the general availability (GA) of new confidential computing VMs leveraging state-of-the-art AMD security technologies offered by EPYC processors and new GPU-accelerated VMs. Additionally, Amazon Web Services announced the new memory optimized instances powered by EPYC processors.

- AMD announced that AMD Pensando data processing units (DPUs) will be one of the first DPU solutions to support VMware vSphere 8 with Distributed Services Engine capabilities running on servers from leading vendors including Dell Technologies and HPE.

- AMD launched the Ryzen 7000 Series processors for desktop, delivering dominant performance and leadership energy efficiency. Powered by the new "Zen 4" architecture, the Ryzen 7000 Series processors feature up to 16 cores and 32 threads and are built on an optimized, high-performance 5 nm process node. AMD also announced the new Socket AM5 motherboard.

- AMD announced the Ryzen 7020 Series processors for mobile applications, bringing high-end performance and battery life to everyday users.

- AMD announced a strategic collaboration with global mobility tech company ECARX to collaborate on the ECARX digital cockpit for next-generation electric vehicles, the first in-vehicle platform to be offered with AMD Ryzen Embedded V2000 processors and AMD Radeon RX 6000 Series GPUs along with ECARX hardware and software.

- AMD introduced the Ryzen Embedded V3000 Series processors, adding the high-performance "Zen 3" core to the V-Series portfolio to deliver reliable, scalable processing performance for a wide range of storage and networking system applications.

- AMD and Energy Sciences Network (ESnet) announced the launch of ESnet6, the U.S. Department of Energy's next generation network to enhance collaborative science. AMD Alveo U280-based network accelerator cards bring powerful adaptive computing to ESnet6, enabling deep insights, rapid detection and correction of problems, and continuous innovation across the network.

- AMD and Samsung announced the second generation of its SmartSSD, powered by AMD Versal Adaptive SoCs, enabling efficient data processing for the data center by integrating the compute and storage functions.

- AMD announced its 27th annual Corporate Responsibility Report, demonstrating its commitment to advancing computing to help solve the world's most important challenges and detailing its progress toward environmental, social and governance goals.

AMD's outlook statements are based on current expectations. The following statements are forward-looking and actual results could differ materially depending on market conditions and the factors set forth under "Cautionary Statement" below. AMD's fourth quarter is a 14-week quarter.

For the fourth quarter of 2022, AMD expects revenue to be approximately $5.5 billion, plus or minus $300 million, an increase of approximately 14% year-over-year and flat sequentially. Year-over-year and sequentially, the Embedded and Data Center segments are expected to grow. AMD expects non-GAAP gross margin to be approximately 51% in the fourth quarter of 2022.

For the full year 2022, AMD expects revenue to be approximately $23.5 billion, plus or minus $300 million, an increase of approximately 43% over 2021 led by growth in the Embedded and Data Center segments. AMD expects non-GAAP gross margin to be approximately 52% for 2022.

43 Comments on AMD Reports Third Quarter 2022 Financial Results

First:then the truth, huh, Su:Buuut, what, Su:Wait, now, were you also (over) confident on your early forecast for today's earnings report, Su?! Wt... :laugh:Well, after the election, many things will change this forecast... again, guaranteed!

Did AMD specify which part of that $1.6 billion was graphics?AMD's Q2 was highest ever single quarter by the company.

Even in Q3, their revenue is record high and margin beats NV's (which dropped it).

Are they really so constrained in TSMC that this was all they could get? They really painted themselves in a small corner, and all the gains of years of supremacy of Ryzen over Intel products have brought them very little, and could be reversed with Intel just on par.

And right now it doesn't really matter what they do or have. We're just in the opening stages of the recession, what the PC industry is now feeling was just return to normal from high demand due to lockdowns. We haven't seen the results of a real market slowdown.

Also, TSMC is really vulnerable right now - almost all high end western products come from there, and embargoing China from ordering such products will surely endanger it, I predict disruptions - either from limiting Chinese exports to Taiwan or entire West, or maybe even from a direct attack (cyber or physical).

A cold shower doesn't hurt them.

I suppose it only costs a couple tens of millions of $ to develop an additional smaller variant (design, verification, masks etc). Maybe I'm totally wrong. It would be nice if we could have some reliable data.

With a dual-core chiplet they will be able to offer:

Ryzen dual-core with 1 chiplet;

Ryzen quad-core with 2 chiplets;

Ryzen hexa-core with 3 chiplets.

Not surprised about the weak client revenue. Think a lot of tech companies are in for a huge reality check over the next year as bust follows the boom that happened during Covid.

Pardon, "Tax optimization".

I'm under the impression that for AMD, the "low end" is just old gen. Zen 2 is not EOL.

AMD Ryzen 7000 mobile series now confirmed to feature Zen4, Zen3 and Zen2 CPUs - VideoCardz.com

Meanwhile intel is making Alder lake Celeron, but they don't have to compete with Apple/nvidia/qualcomm etc... For allocation. Owning your own fabs do have benefits after all.

Nooo :kookoo:

AMD Ryzen 5 3600X ab 139,90 € (November 2022 Preise) | Preisvergleich bei idealo.de